Everyone can benefit from having a budget – no matter your current financial situation. Why? A budget is a tool to focus on what money comes into your household each month, and how you spent, saved, paid down debt, or donated to a good cause. One of the most significant benefits of a budget is that you can accurately plan for your desired financial goals.

Budgeting is a tool to help make conscious decisions about where you spend money and in what amounts, and ideally dedicate funds to your savings goals. Even if your income is irregular or unpredictable, it’s worth taking time to create a plan for your money and try to stick to it as best as possible.

We’ll break down how to make a budget with just three main spending buckets so it’s easy to follow. Let’s explore how to make one!

Understand your monthly income

First, you need to know how much money is coming in after you pay taxes. Ideally, you’ll have a recurring figure that comes in, but that may not be the situation for everyone.

For anyone who is salaried, understanding monthly income is simple. Review your most recent pay stub and find your net pay (after deductions and taxes). To determine your monthly income, multiply your net pay by the number of direct deposits or checks you receive during the month.

If you work on an hourly basis, your paycheck may vary each time. If you’re budgeting in this way, you can work off of the lowest amount you’re likely to receive in a month, or review past paychecks and calculate your average monthly earnings.

For those who earn commissions, bonuses, or tips as part of their main job, calculating monthly income is trickier due to the ups and downs of these types of compensation. If you’ve held the same position for a while, you can more safely estimate the amount you’ll earn from commissions, bonuses, or tips.

Do you earn money from other sources, like rideshare driving, tutoring or babysitting? If this money helps you pay your bills, make sure to factor it in to your monthly budget. But, if you do this work just for extra spending money or savings, or infrequently, you may not want to rely on it for your monthly budget.

Calculate recurring expenses

Next, you’ll need to understand and calculate your recurring expenses – these are things you’ll pay for on a regular basis. It’s usually monthly, but some services or bills are quarterly, biannually, or annually.

Some will be the same dollar amounts each month, like your rent or mortgage payment. Others vary based on usage, like your electric bill. Here’s a list of common recurring expenses:

- Rent/mortgage payment

- Renter’s/homeowner’s insurance

- Utilities – electric, gas, water, trash, internet, phone

- Health insurance premiums

- Car payment

- Car insurance payment

- Childcare

- TV/entertainment (cable, streaming services, gaming subscriptions)

- Education loan payment

- Gym membership

- Other bill(s) you pay every month

Add a dollar figure beside each recurring expense to your situation to calculate your monthly recurring costs. Understanding how much of your income is spent on these items is essential because the money you spend on recurring expenses is challenging to change in the short term.

Non-recurring expenses

Non-recurring expenses are as important to your daily life as recurring ones – these are things you need, but they don’t come with a fixed cost and a due date for the bill. The big difference is that you have a bit more control over the timing of these expenses and how much you spend in the short term. The most common of these are:

- Groceries

- Gasoline

- Doctor visits

- Medications

- Veterinarian visits

- Car maintenance & repairs

- Clothing

- Household items and appliances

- Other non-recurring expenses

Go through your most recent debit and credit card statements to assign a typical monthly dollar figure for each of these expenses, then add them to calculate your monthly non-recurring costs.

Review your monthly discretionary purchases

Last, you’ll have a category of purchases that covers non-recurring, optional purchases. Make a list of discretionary purchases that you make in an average month, including:

- Restaurants/bars

- Takeout food

- Kids’ activities

- Entertainment (movies, sporting events, concerts, etc.)

- Travel

- Gifts

Again, most of these purchases likely hit your debit and credit card statements. But, if you use cash, you may need to review receipts or rely on memory. Add them up to see how much you spend on discretionary items. Some bigger purchases like hotels and airfare for travel likely occur only a few times a year, so you may need to estimate the monthly cost.

This is the group of expenses over which you have the most control to reduce your spending in the short term, possibly eliminating some items altogether.

Review expenses vs. income

Congratulations! You have collected the information needed to create your first budget. You know your actual income and expenses for a month. Now it’s time to see how your expenses and income match up. Start by taking the amount of your monthly income and subtract the three categories of expenses – recurring, non-recurring and discretionary. The remaining amount is a monthly increase/decrease in your cash (deposit) account.

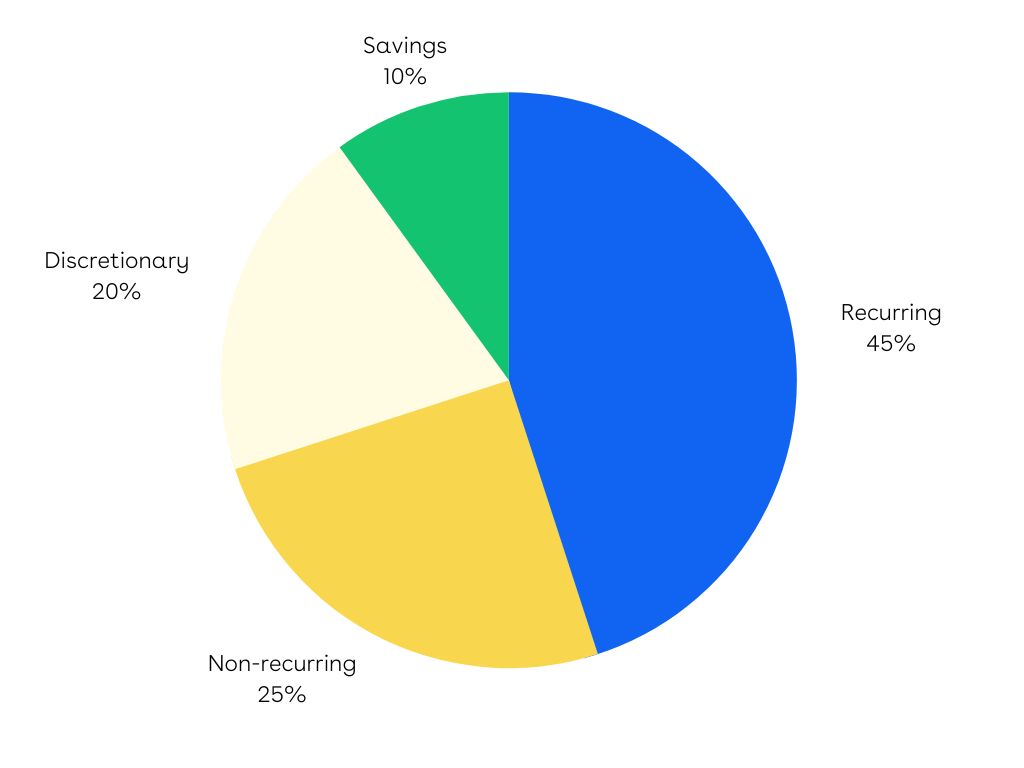

You may want to visualize what categories are taking up space in your budget. Here is a sample pie chart to illustrate:

What happens if you are spending more than you’re bringing in? Calculating a negative figure is possible. No need to panic if this is your situation. But, your priority should then be reducing spending in the short term and finding ways to increase your income.

If you have more income than expenses, that is a fantastic start! Your priority would then be to make a plan for the extra funds – such as setting a saving goal. You could build an emergency fund and work toward a long-term savings goal, like retirement, and a short-term savings goal. Try to choose something fun that will encourage you to stick with it.

Whether you are earning enough to cover your expenses or not, consider how you would like to change those figures to achieve your ideal situation. Whatever your priorities, you can use the information from your budget to help guide you to make choices that will help you progress toward what brings you the most fulfillment.

Track your budget

By comparing your expenses and your income, you understand exactly where your money goes, and can make a realistic budget. But, you’re not done. The next step is to stick to that budget!

Put the amount allocated for each category – recurring, non recurring, discretionary, and savings in a spreadsheet. Track your spending in each category monthly. Or, if you have a hard time staying on track, you might want to do a mid-month check in. That way, if you need to cut back in an area to stay on budget, you know before it’s too late.

The goal is to stay within the budget by spending less than what you’ve allocated in your three spending categories so you have more left over to save. By tracking your spending, it helps build and reinforce habits that will support your own goals.

Conclusion

If you’re new to budgeting, it’s smart to break your budget down into a smaller number of buckets so you can more easily keep track. This way, you can visualize your situation and make choices accordingly. You can always customize it and get more granular once you’re comfortable with your budget!

Keep reading on the Milli blog:

How to Cover Unexpected Expenses

Aspirational Spending: What is it, and how to Combat It

6 Tips to Keep Track of Bills and Payments