When you think of the phrase “building wealth,” what comes to mind? You might envision a substantial balance in your 401(k) and Roth IRA accounts, owning property, or a brokerage account with a diversified portfolio of stocks and bonds. All of those options are fantastic, but don’t overlook another player in the game: the humble savings account.

A savings account? Is that too basic? We know, it feels like finance 101! Though using a savings account is a fundamental step in the journey of mastering personal finance, savings accounts with high interest have come back in style as a truly meaningful way to meet your financial goals.

In this blog, we’ll dive into why using a good old-fashioned savings account to keep some of your money in cash may be more advantageous than you thought. Spoiler: if you’d like to see your money grow, keep reading.

Benefits to Using a Savings Account

First, let’s cover what makes a savings account so great – regardless of whatever interest rate a savings account offers (because that changes over time). Here are some of the key benefits:

Security

A savings account provided by a bank is safe and secure. Thanks to the FDIC, member banks that offer accounts have insurance (usually $250,000 per depositor account), so even if the bank fails, you won’t be at risk of losing your money.

Liquidity

With a savings account, you’ve got easy access to your money. It’s liquid – meaning you can withdraw it at any time without penalty. Other investment options like Certificates of Deposit may have restrictions or penalties for early withdrawal.

No loss of principal

Savings accounts are secure in another way; because your money is liquid and earning interest, the balance of your account will (most likely) only go up. So long as you’re not paying fees that eat into your balance, your account should continue to grow each month. Unlike a share of stock or bar of gold that can change value, a savings account does not fluctuate. And because of this steadiness, you can more accurately predict when you’ll reach your financial goal. Interest rates can shift, which can speed up or slow down the time it’ll take to accrue interest to reach your goal. But, you won’t have to worry about a major setback because of a swing in the market – and that peace of mind is priceless!

Easy to automate

Do you like convenience or need some help to save? Setting up automatic savings

or direct deposits from your income to your savings account can help establish a routine. This automated approach makes it easier to save consistently without relying on willpower alone.

For example, with Milli, you can create a “set and forget” Savings Rule to automatically transfer money from your Spending Account to your Savings Account or Jar on a daily, weekly, bi-weekly, or monthly basis.

Savings Accounts are Cool Again

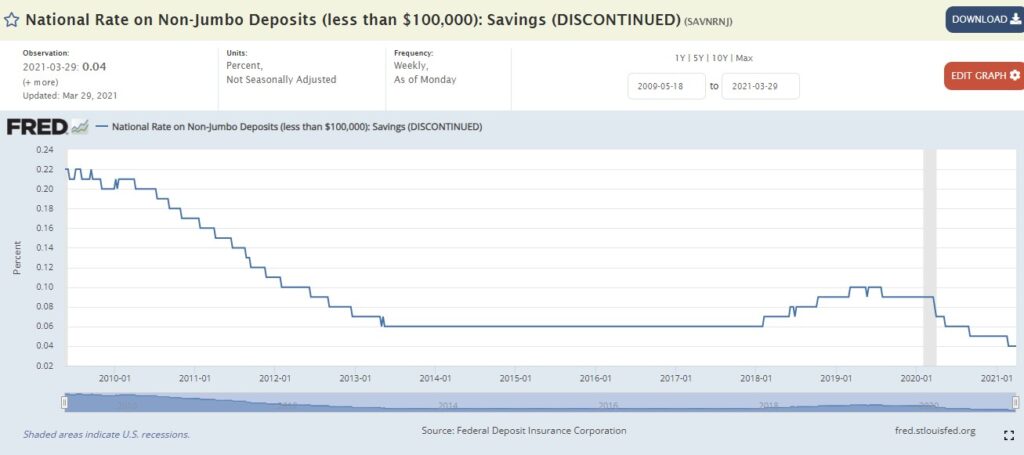

In the (not-so-distant) past, savings accounts offered Annual Percentage Yields (APY*) that were significantly less than inflation. Between 2013 and 2018, there was a period of economic growth for the United States as defined by GDP, the cumulative rate of inflation was 7.8%.

At that time, the national interest rate on deposits under $100,000 was stable…at a whopping 0.06%. On a $100,000 balance, that would mean earning merely $60 in interest per year. Not the most compelling option!

If someone were to have put their money in a savings account during the 2013 to 2018 period, they would have less buying power each year because inflation far exceeded the interest earned on their money. In that scenario, someone looking to grow their wealth would have to check out alternative options to using a savings account.

But thankfully, things are shaking up in the world of interest rates. Since March 2022, the Federal Reserve has steadily raised interest rates to curb inflation. That means more money borrowers will have to pay back for their loans. (Sorry, first-time homebuyers who didn’t lock in a 3% mortgage a few years ago.)

For savings accounts however, that’s good news! It means more interest is being paid on whatever money is in the account. And that’s truly passive income.

Right now is the sweet spot; as reported by the Bureau of Labor Statistics, inflation is easing as consumer prices drop in some areas and slow down their growth in others. But, interest rates are still high, so using a savings account is a better deal than in years past. Keeping money in a savings account no longer means automatically losing buying power from one year to the next!

Stock Market Volatility

Another factor that makes savings accounts so attractive is that more guaranteed return, which is extra important at a time when the alternative options are more volatile.

Investing does involve the risk of losing the capital – whether the share price of a stock you’ve purchased declines, or you invest in a rental property that faces storm damage or tenant problems. There’s simply no guarantee you’ll get a positive return on your investment.

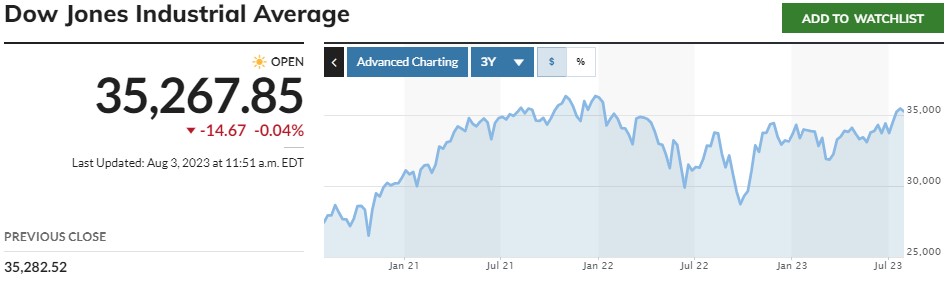

While the stock market delivers long-term returns on average, the market has been especially volatile in the years since the coronavirus pandemic hit. Supply chain constraints, the Great Resignation, inflation pressures, and more have made stock prices fall, rise, fall, and then creep back up making the charts look more like a rollercoaster than a ramp.

As of July 20, 2023, the Dow Jones Industrial Average, NASDAQ Composite Index, and the S&P 500 Index have not reached the peak that they reached in October/November 2021. (Of course, any one person’s individual return will be unique to them based on what they have chosen to invest in. Maybe you have a knack for only choosing the best investments!)

Long term investors know the stock market has its ups and downs and are aware of the storms they may have to ride out over time. But for some, it can take years to ride out the losses. Good news is, that’s not a big deal for younger investors who have time for the market to rebound before retirement or, for wealthier investors who can afford a dip in their portfolio. If you don’t need the cash you’ve invested anytime soon, then you likely have more tolerance for risk on volatility.

When would it be a good idea to put your money in a savings account alongside investing it?

But what if you aren’t young with time to spare or you don’t have a substantial savings cushion? If you need (or might need) immediate access to the cash from your investments, it may be more helpful and reassuring to have more of your money in cash. Perhaps you have retirement coming up, or a large purchase where you don’t want to jeopardize your ability to cover the expense.

That’s where that humble savings account comes in to save the day!

With a high-yield savings account, or even laddered Certificates of Deposit (CD), you can earn interest on your money at a return you can more predictably calculate. High yield savings accounts are great if you need flexibility. Shameless plug: Milli’s Savings Account and Jars can help you save and budget for specific expenses along the way to reaching your financial goal.

Conclusion

Just like fashion trends, strategies to build wealth and manage money go in and out of style. Not long ago, savings accounts earned basically nothing in interest while there was a steadily growing stock market. But now, the situation is quite different. Savings accounts are offering interest rates that can meaningfully grow your money!

Ultimately, there’s no all-or-nothing, one-size-fits-all approach to building wealth. If you’re still unsure of what to do next, consider working with a financial advisor to plan based on your needs, goals, income, assets, and current expenses.

If you’re looking for a savings account with a competitive APY, check out Milli. We offer a highly competitive rate and our Jars and helpful savings automations make it easy to save. Download Milli from the App Store or Google Play!

Keep reading on the Milli blog:

Does Couponing Really Save you Money?

4 Benefits of a Mobile Bank

Top Banking Terms You Should Know