Is there a good time to start saving for retirement? Yes – as soon as you earn your first paycheck! Since that’s probably already in the past for you, we’ll go with the next best option – today.

It may feel like you can delay it when retirement is in the distant future, but that’s precisely why you should start as soon as possible. Most financial professionals advise starting to save for retirement as early as possible to give yourself more time to earn more and contribute to your retirement accounts, but also for the money to grow and build on itself from investments.

Saving for retirement is a big feat that involves unpredictable factors, timing and education with the market, and navigating different account types and tax strategies. Plus, the stakes are high, because you’re preparing to have the money you need for a stage in your life when you may not be able to work. It can feel overwhelming. But fortunately, saving for retirement is manageable once you break it down!

We’ll dive into some retirement savings projections, types of retirement accounts, and how much you should aim to save.

Retirement Projections

Why is it so important to start early? Is it really worth saving for retirement when there are other more pressing expenses and life events in the near future? Let’s explore some retirement savings scenarios to show why it’s seriously worth carving out some of your paycheck for retirement:

William is 18 years old and starting with no retirement savings. Right now, he can dedicate $2,400 per year – $200 per month – after his other expenses. If he contributes $2,400 per year to a Roth IRA (individual retirement account) between the ages of 18 and retirement at 65, he will contribute $112,800. But with an expected rate of return of 7% on the invested funds, he will amass over $790,000 in that account.

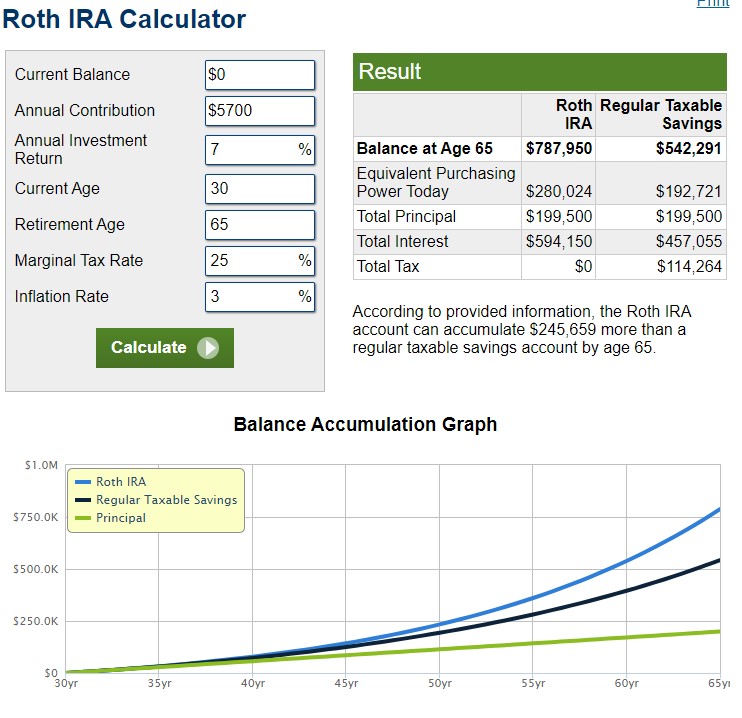

See how it’s broken down from Calculator.net’s Roth IRA calculator:

Ana is 30 years old and knows she needs to start seriously saving for retirement. She has nothing in her Roth IRA, but can contribute $5,700 per year. If she keeps that up until age 65, she’ll contribute $199,500 – a lot more than William. But with the same 7% rate of return, the account balance will be similar at just under $788,000.

Ana is still getting great growth by starting to save when she can! But, William’s head start means he can contribute a lower amount overall and monthly and still come out ahead of those who start saving much later. And, if he can contribute more to his retirement as his financial situation allows, he’ll be able to compound on his earlier efforts and end up with even more money in his retirement account.

Of course, there are more factors to consider in your decision about how much to dedicate to retirement, and we’ll dive into those soon! Ultimately, the key point is that starting as soon as possible can pay off decades down the line, even if the contribution doesn’t seem like a lot.

Types of Retirement Accounts

Now that we know why it’s so important to start saving for retirement early, let’s dive into the most common retirement accounts. There are two – 401(k) accounts and IRAs (individual retirement accounts). They each have their own unique features, benefits, and rules.

401(k) accounts

If you’re hearing about retirement plans at work, chances are you’re hearing about a 401(k) retirement plan. It’s the most common employer-sponsored plan, and it’s named after the relevant section of the Internal Revenue Service (IRS) tax code.

How does a 401(k) retirement help you save for retirement differently than if you were to put the money in a savings account? 401(k) plans are invested in various things like stocks, bonds, and mutual funds. Usually, there is a plan servicer that handles the details. You’ll likely choose the target date you plan to retire, and they will invest on your behalf accordingly. Many people use this strategy, but it may not be best for you – it’s worth speaking with a financial advisor about the best choices for your needs.

Each year, there is a limit to how much someone can contribute to 401(k) plans. In 2023, it’s $22,500 (IRS) for people age 49 or younger. People 50 or older can contribute an additional $7,500 per year as a “catch-up” contribution. The earliest someone can withdraw the funds without penalty is age 59 ½, though there are a few exceptions for some specific, extreme hardships.

There are several crucial things to know about these accounts for those looking to save for retirement:

- Money saved for retirement in many 401(k) plans are done on a tax-deferred basis. (Some plans offer post-tax savings options).

- Many employers match part of the money you save.

- The amount you’ve contributed to your 401(k) plan moves with you when you take another job, but some of the employer matching contribution may not have vested and you may have to forfeit it.

Tax-deferred basis

The government wants to encourage you to take responsibility for saving for your retirement. It does so by providing the significant benefit of tax deferral on money you save for retirement within a 401(k).

Retirement savings in a 401(k) account are “pre-tax” or “tax-deferred” which means they are not subject to taxation at the time you deposit them into the account. So, if you earn $50,000 in a year and deposit $5,000 into a 401(k), you’ll only owe income taxes as if you earned $45,000 of income for that year.

The tax-deferral advantage of a 401(k) account also applies to investment earnings on the account. But, since you don’t pay income taxes on the money when you contribute, you’ll pay income taxes on what you withdraw from the 401(k) when you do so in your retirement. For some, that works out in their favor because their tax bracket is lower in retirement than when they were at the peak of their career.

It’s important to remember that tax codes change and adjust over time with inflation and legislation. It’s impossible to predict exactly how much income taxes will be in your retirement. So, the farther away from retirement you are, the more you should focus on simply accumulating more funds. But when retirement is much closer on the horizon, set up a meeting with a financial advisor to go over the specific investment, withdrawal, and timing strategies that will serve you best – it’ll be time well spent.

Employer matching

Who doesn’t want more money from their job? Another key reason to save with a 401(k) is that many employers match a portion of the money you save for retirement, but only if you save with the company’s 401(k) plan. It goes straight to the 401(k) account, so it’s also tax-deferred.

There are any number of formulas that companies use to determine the matching amount. For some, they match 100% dollar-for-dollar up to 3% of the employee’s salary. Others will match 50% of the first 6% of the employee’s salary. Some will make a one-time annual contribution of a certain percentage. You’ll need to ask your human resources team for the details of your company’s plan.

The other important part about employer matching is that it allows you to contribute beyond the limit of what the employee can add in. The total limit for contributions to a 401k account is the lesser of 100% of the employee’s total compensation, or $66,000 for 2023.

Make sure you understand how much you need to contribute to get the full match from your employer and prioritize saving that amount, so you don’t leave compensation on the table!

Retirement savings are portable

Even though retirement savings in an employer-sponsored 401(k) plan are managed by the provider the employer chooses, the money is portable. If or when you move to another job, you can keep the funds in the same 401(k) plan, or migrate or “roll over” the funds to a new retirement plan – such as the 401(k) with your new employer, or an IRA.

The portion of the money your employer contributes to the plan may be subject to a vesting schedule as an incentive for you to stay with your current employer, but all funds contributed by an employer must be 100% vested within five years. Many employers treat employer contributions as 100% vested immediately. Check your employer’s plan to understand whether vesting is immediate. When employer contributions are fully vested, that money becomes yours and is portable, just like the portion you saved.

IRAs

But what about saving for retirement outside of an employer plan? Individual Retirement Accounts (IRAs) are another type of retirement savings account that is not connected with an employer. Anyone with earned income can establish an IRA at a bank or brokerage – even if you also have a 401(k) plan with an employer.

In 2023, the IRA contribution limit is $6,500 for anyone age 49 and younger. For people age 50 and up, the contribution limit is $7,500 – designed for those closer to retirement to catch up on their savings. However, if you are single or married but filing your taxes as single, you cannot contribute more than 100% of your taxable income to the IRA. So, if your taxable income is less than the $6,500 or $7,500 amount in a year, you are limited there. If you’re married and filing taxes jointly, your spouse can contribute to your IRA for you from their income.

There are multiple types of IRAs – but the two most common are Traditional and Roth. A Traditional IRA allows you to save on a tax-deferred basis, like a 401(k). But, there are income limits that apply, and they vary whether you have access to an employer-sponsored retirement plan; get the details from the IRS here.

A Roth IRA funds the account with dollars that have already been taxed. But, earnings on the account are tax-free; no tax bill comes due when withdrawals are made in retirement. There’s one caveat; to get the tax-free growth, the withdrawal has to come five years after the first contribution. (So, another reason why it’s so valuable to start early!) The Roth IRA is a good choice for a person who wants to have retirement funds free and clear of future taxes.

High earners, watch out – there are also income limits to using a Roth IRA, and they depend on if you are single or married. Luckily, they do increase every year to adjust for inflation. For 2023, single filers earning $139,500 and married filers earning $219,000 or more combined start to hit the threshold where they can’t contribute the full amount. (If you’re lucky enough to be in this position, you may want to seek guidance from a financial advisor about other ways to invest so you can still set up your financial future!)

With an IRA, you can be a bit more hands on than with many 401k plans. Either independently or with a financial advisor, you can choose which funds to invest in. This flexibility is great for seasoned investors or those who want to invest in specific regions or types of businesses.

How much to save for retirement

So now that you know about the different retirement savings options, you may wonder – how much should you save? In general, the more you save, the better, but you already know that!

What’s a more helpful target to shoot for? Fidelity, an investment and retirement account provider, recommends saving 15% of your pre-tax income per year for retirement.

So what if you can’t save 15% – where do you start? As we mentioned earlier, a great start would be to contribute enough to get the full match from your employer’s 401(k) plan, should they offer one. By having the funds deposited to the 401(k) account before they hit your bank account, it feels like you’re automating the savings because you don’t have a way to spend that money. If you don’t have access to a 401(k) plan or want to contribute more, the Roth IRA can be a great option because of the tax-free growth. From there, your next options are to increase your income and reduce spending so you can allocate more money to retirement.

But what about a dollar figure to shoot for? Typical wisdom is to save $1,000,000 and follow the 4% rule. That means investing it for a conservative growth target of about 4%, and withdrawing $40,000 per year without fear of running out of money. And even if you kept $1,000,000 in cash and withdrew 4% each year, it would last 25 years.

But, $1,000,000 has less and less buying power over time. $1,000,000 if you retire in 2023 will provide a much different lifestyle than someone retiring in 2053. It’s also less helpful, one-size fits all guidance because everyone has different lifestyle and financial needs. T. Rowe Price recommends that by age 65, you have 11x your pre-retirement gross income saved and invested. That reflects the cost of living in your area and your unique lifestyle.

For your specific situation, you’ll need to assess your financial needs in retirement. Here are some things to consider:

- How long do you plan to work?

- How long is the life expectancy of someone in your ethnic group and biological sex at the year of your birth?

- What does your family medical history tell you about how long you can expect to live?

- Will you have a housing payment in retirement, or will you have a paid off house? How much will property taxes be and grow, if you own property?

- Do you live in an area with a higher or lower cost of living for things like food and transportation?

- Do you have family who can aid in caretaking as you age, or will you need to factor in the cost of home aides?

Explore an online 401k calculator and Roth IRA calculator with your specific details to get a better picture of what retirement savings you could accumulate by investing at different amounts. If your financial situation allows, and can leverage both a 401k for a tax-deferred account and Roth IRA for tax-free earnings, you’ll maximize the complementary benefits.

Conclusion

Retirement is a special time to relax after time in the workforce and spend time doing what you enjoy most. Part of a great retirement means having the money to live the life you want, and that involves some preparation!

Now, you’re informed with information about the most common account types, basic rules, and target amounts to save. You can go forward and start taking steps toward building a retirement nest egg.

We get it – saving for retirement provides a reward that is often quite distant, especially when you likely have pressing financial needs in the present. It’s all about building the mindset that you’re serving your future self.

Hopefully, the tax-deferral and employer match benefits provide some short-term motivation to start saving. You will get excited when you see how quickly a retirement fund balance builds. And when you’re ready to retire, you’ll appreciate that past-you put aside some money!

For ideas on how to dedicate more room in your budget to save for retirement, check out these blog posts: