Are you ready to take control of your financial future and protect your health? Look no further than the power couple of a substantial health insurance policy and supplemental insurance policies. Together, they form a strong shield that can ensure both your physical and financial wellbeing.

Medical insurance is the foundation of your healthcare, providing coverage for medical expenses, prescriptions, and hospital stays. But don’t stop there – there are other supplemental types of insurance you can purchase to level up your financial security. These specialized policies are designed to fill the gaps left by traditional health insurance coverage or provide cash benefits to help you address other needs while you focus on recovering from an accident or illness. The best part is that many of these supplemental insurance plans have very low monthly premiums – they can be as low as a latte, so it’s feasible to make room for them in your budget.

Looking to build out your financial safety net with more robust insurance coverage? Here, we’ll cover the many types of insurance related to your health so you can see which might meet you or your family’s needs.

Health Insurance

Let’s start off with the primary form of insurance for your wellbeing and medical care. Depending on your plan, health insurance will cover expenses (or part of the cost) for things like:

- doctor’s visits

- medical tests

- hospital stays

- surgeries

- prescription medications

- vaccinations

You may have your health insurance through a PPO (Preferred provider organization) or an HMO (Health maintenance organization). With an HMO, it’s a tighter-knit health system and you can typically only get coverage within the organization. With a PPO you typically have more choices when it comes to providers and facilities, and providers can accept multiple forms of insurance. If you build relationships with your doctors and your insurance changes, you may still be able to continue care with them.

In the United States, people can access health insurance through private (such as through your employer) or public options. In 2021, private health insurance was still more prevalent than public options. If you’re purchasing health insurance through the marketplace, the open enrollment period for the next year begins in the fall the year prior; for 2024 the open enrollment begins November 1, 2023. Or, you can get a special enrollment if you’ve had a qualifying life event.

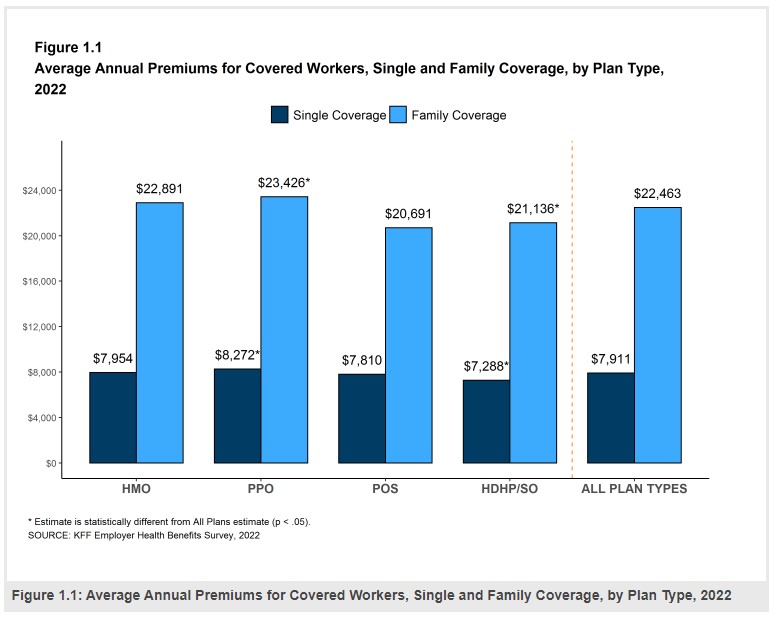

Health insurance can be a big percentage of a person or family’s budget, with the average premium for single person coverage coming in at $7,911 per year, and $22,463 for a family of four. The amount you’ll pay largely depends on how you access insurance, such as a benefit plan from your employer.

It can be challenging to lower costs on private insurance because you may only have the employer plan options to choose from. If you are looking to lower your healthcare costs without sacrificing coverage, you may consider finding a new job with a stronger health insurance benefits package, or leveraging tax credits, if you qualify.

Be sure to understand what your plan covers and re-evaluate it every time you go through a new health insurance enrollment. A typical medical insurance plan doesn’t cover everything, so let’s dive into a few more specific types of health-related insurance.

Dental Insurance

Teeth may be part of your body, but primary health insurance typically doesn’t cover dental care. Dental insurance can cover your routine exams and cleanings, x-rays, and more substantial dental work like fillings or root canals. Sometimes it covers orthodontia, or a limited amount toward orthodontia.

You can access dental insurance through your employer or purchase it directly from a dental insurance company, and often there is no waiting period to access care. If you don’t have dental insurance from your employer, you can expect to spend $20-$50 per month on the premium. If you get a plan with a decent premium that covers at least preventive care (like those two annual visits to get your teeth cleaned) it can be cost-effective compared to paying for office visits out of pocket.

Vision Insurance

Vision insurance covers care for your eyes and eyeglasses or contact lenses if needed. Even if you don’t currently wear glasses, it’s important to get your eyes checked annually. Eye exams can help detect potential problems early on which can help preserve your vision or help you identify if you do start to need glasses.

However, paying out of pocket for vision care is less dramatic of a cost compared to most medical or dental appointments. Retailers including Target Optical, Costco Optical, and the Vision Center at Walmart have independent doctors of optometry on-site that conduct eye exams, and the cost is often between $50-$100 (expect to pay more for dilation or OptoMap imaging). Direct to consumer glasses companies like Warby Parker, Zenni, and EyeBuyDirect offer glasses that cost much less out of pocket than buying glasses in-store, using insurance. If you don’t have access to a subsidized vision insurance plan through an employer, it may be a breakeven cost to pay for the exam (and some glasses, depending on your selections) out of pocket compared to paying for an individual insurance plan.

Accident Insurance

Accidents happen. The good news is, you can purchase coverage to supplement your primary health insurance specifically for them. Accidental injury insurances provide cash benefits should you experience an accident covered by the policy, like a broken bone. This cash can go toward the cost of medical care, ambulance services, or nonmedical needs.

If your weekend or vacation plans include adventure sports that come with a risk of accidental injury, this can help minimize financial risk. It’s relatively inexpensive – as low as $6 per person per month – and you can request a quote online for an individual policy if your employer doesn’t offer it.

Critical Illness Insurance

Similar to accident insurance, critical illness insurance provides lump-sum benefits should you experience a more serious health problem. Different insurance companies and policies cover different medical events, but it commonly covers medical problems like heart attacks or strokes.

The insurance company will provide the funds to address out-of-pocket costs of care or other life needs, like housing or groceries. This can be especially helpful if you must temporarily or permanently stop working due to an illness.

Hospital Indemnity Insurance

Think you might have an overnight hospital stay coming up? A special subset of insurance is hospital indemnity insurance which provides cash benefits for overnight hospital stays. Whether you’re pregnant, have a chronic illness, or have an upcoming surgery, it’s worth looking into a policy that can cover stays related to these needs because the policy can pay for itself with just one overnight stay.

Disability Insurance

Disability is a spectrum – some disabled people can work, perhaps with accommodations, some need a short time off work to recover from a temporary disability, and others cannot work at all. The Center for Disease Control reports one in four adults in the United States has a disability.

California, Hawaii, New Jersey, New York, Puerto Rico, and Rhode Island require employers to offer disability insurance to employees; if you live in any of these areas, inquire about the plan with your human resources department.

If you’re unable to work due to a temporary or permanent disability, disability insurance can help replace your lost income. There are two types depending on how long you’ll be unable to work.

Short-term disability insurance

The word “disability” sounds severe, so it’s important to keep in mind that some conditions that cause people to take a short-term disability leave from work are both common and not at all life-threatening. The Council for Disability Awareness reports that the most common causes for short-term disability include pregnancy, musculoskeletal problems, injuries, digestive disorders, and mental health issues.

In the case of a short-term disability, insurance can help you take the time you need to recover fully rather than having to return to work prematurely. Short-term disability insurance typically covers 67% of your weekly income, up to a certain number of weeks – such as 13, 26, or 52.

Long-term disability insurance

If you find yourself with a medical condition that causes total disability, typically for one year or longer, that’s when long-term disability insurance would start to provide benefits. Long-term disability typically covers 60% of your monthly income. Different long-term disability insurance plans have different Elimination Periods, which is the length of time the policyholder must be disabled before the plan starts to pay benefits.

Long-term disability insurance is different from disability benefits provided by Social Security, which may also apply – it’s supplemental. Private insurance can be especially helpful if you have not yet met any of the requirements for SSDI, such as the duration of time worked in the period prior to the disability.

Long-Term Care Insurance

As we age, we need more support, and are more likely to need professional caretaking. Long-term care insurance provides coverage for the costs associated with extended medical or support care services, which are often not covered by traditional health insurance or many Medicare plans. As we age, we need more help with daily living activities. According to the U.S. Department of Health and Human Services, about 70% of people who reach age 65 will need caretaking at some point, even if only temporarily.

Long-term care insurance can cover care provided in a variety of settings, including nursing homes, assisted living facilities, adult day care centers, and even in-home care. There are a number of policies to choose from that have different daily or monthly benefit amounts, the maximum benefit period, and the criteria that must be met for the coverage to start, such as the inability to perform a specified number of daily living activities or cognitive impairment. Some policies include inflation protection to make sure that the benefits keep up with the cost over time.

You may be able to pay for the premium through tax-advantaged health savings accounts, which makes it more affordable. Buying long-term care insurance earlier in your life when you have fewer health issues can lower the cost, so it’s worth exploring even if you likely won’t need care for years to come.

Travel Health Insurance

If you’re planning a trip, you may be venturing beyond the service area for your main health insurance, especially if you’re traveling internationally. Signing up for a travel health insurance policy can help cover any gaps. It can cost less than a meal out or attraction tickets for the family. Budget for it when booking a vacation, then spend your trip relaxing instead of worrying about potential storms (literal or metaphorical) that could roll through.

Conclusion

Evaluating your health insurance needs and filling any gaps by enhancing your protection is a smart way to strengthen your financial security. Many supplemental insurance policies have low enough premiums where you likely won’t miss the additional $10 to $20 each month, but you will notice the meaningful benefit if you do ever need the policy.

Take some time to review your insurance needs periodically, adjust as life changes pop up. Invest in comprehensive health and supplemental insurances today for peace of mind!

Keep reading on the Milli blog:

Financial Planning for Your Children and Family’s Future

Virtual Cards: The Upgrade Digital Payments Have Been Waiting For

How a Savings Account Can Help You Reach Your Financial Goals