What’s a “normal” or typical amount of money to have? What sort of net worth do people across the United States have? How does it change over time, by year and by life stage? You may wonder about the financial status of your peers – perhaps you’re looking for a benchmark to compare your own financial situation, or sheer curiosity.

There’s no clear answer because money and wealth are held in many forms – cash, stocks, property equity, and other assets. An individual or family’s net worth is determined by the total assets they have (money and property) minus their liabilities, like balances on loans. To get an idea of how much money your peers have, we’ll need to take a deeper dive.

Let’s review the data from the United States Census Bureau and the Federal Reserve Board to dive in to how much money and net worth Americans have, looking at it from multiple perspectives.

A quick refresher on averages: We’ll be analyzing these numbers by the median, which means half of survey respondents (individuals or families) have more, while the other half have less – so it’s a good way to see what’s “typical.” Usually when people look at the average of a group of numbers, they look at the mean, but that tends to skew higher because of a few outliers on the upper end. In this case, that would mean that a small subset of survey respondents with extreme wealth in each category would disproportionately inflate the numbers. We want to provide a realistic midpoint, so we’ll stick with the median.

Get ready for lots of charts!

Americans’ Net Worth

First, let’s look at the net worth for all families. The United States Federal Reserve produces a Survey of Consumer Finances every three years with the most recent edition coming out in 2022. In 2022, the survey found the median net worth for American families was $192,700.

We can see that back in 2007, the median net worth was $173,150 (adjusted for inflation – the figure is in 2022 dollars), followed by a decline with the 2008 recession caused by the housing market crash. That set the median net worth back to about where it was in 1992. Luckily, it’s now back to above where it was, so as a country we’re collectively on the upswing!

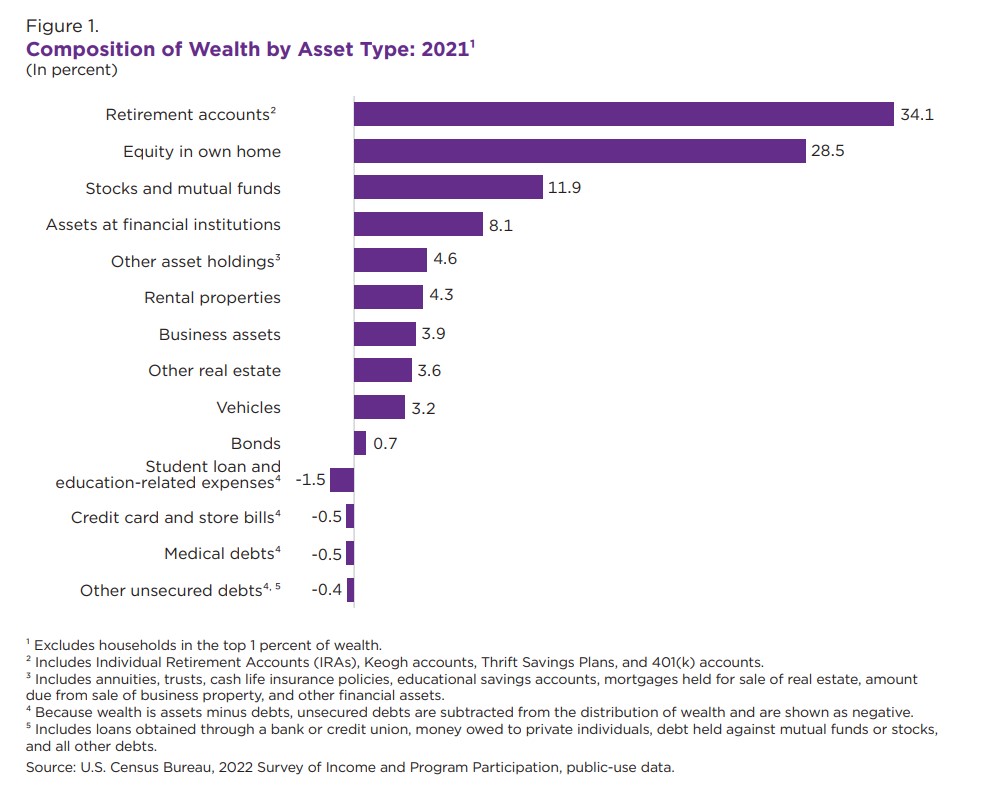

Now, let’s dig into some other considerations to give us a better view. Since we saw that the net worth of all families was impacted heavily by the 2008 housing market crash, let’s look at Americans’ net worth by housing status. Net worth ties in with property ownership, as the U.S. Census Bureau’s Survey of Income and Program Participation found that property equity is the second highest component of wealth for Americans, behind retirement accounts. The median home equity was $174,000 in 2021 dollars. For the 7% of Americans who own a rental property, the median value of that was $200,000.

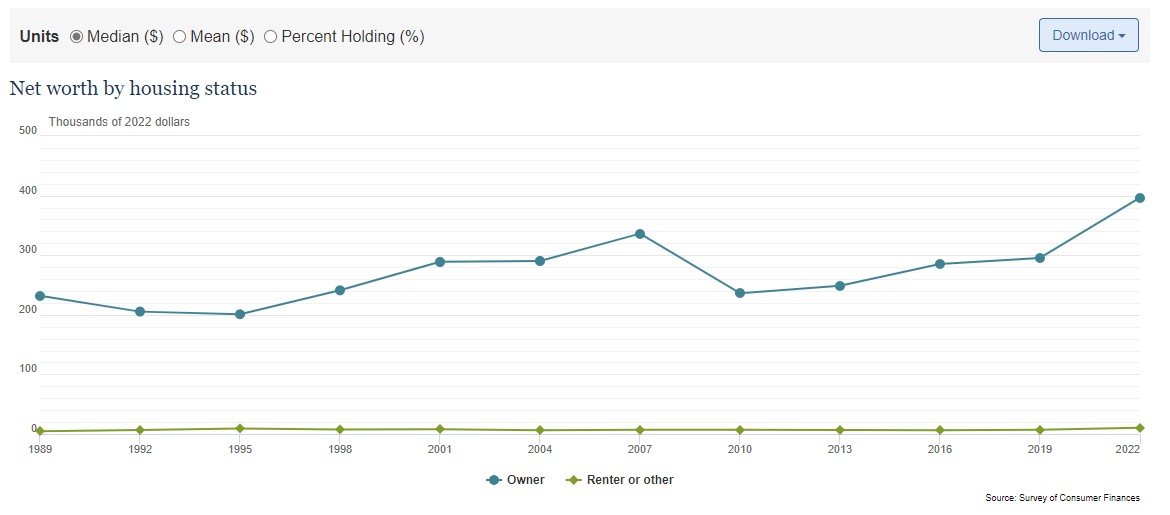

In 2022, the net worth of homeowners was $396,500, and $10,410 for renters – a stark difference. We can also see the net worth of those who rent their housing has remained relatively flat, from $4,610 in 1989 to just over $10,000 in 2023, whereas homeowners have seen much larger gains in net worth due to rising property values increasing their equity. Owning a home is a clear vehicle for growing wealth; even when the housing market crashed in 2008, the median net worth of homeowners in 2010 was still over $230,000 more than renters.

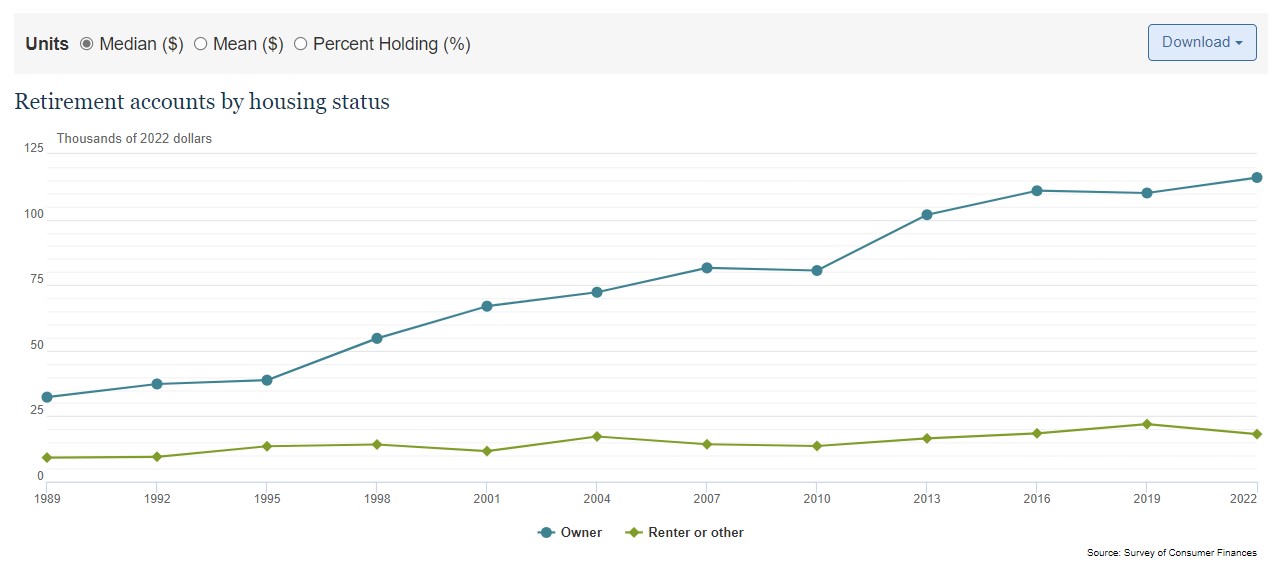

This may be surprising after seeing the earlier chart from the Census Bureau survey that found the primary composition of wealth is retirement accounts, not property. How’s that? It’s entirely possible to build wealth while renting through avenues other than home equity, such as retirement accounts, the stock market, or owning a business. However, the data shows that even the balance in retirement accounts by housing status differs. Homeowners have a median retirement account balance of $116,000 while renters have $18,190 (down from a high of $22,000 in 2019).

What might be causing this? Why don’t more renters have a higher net worth, if they can leverage the same accounts to save for retirement? A likely factor is that their housing cost climbs with regular rent increases, which impacts renters’ ability to save and invest. In comparison, homeowners with a mortgage usually have a flat housing payment, and over 39% of American homeowners have a paid-off home. That can allow homeowners to dedicate extra money that would otherwise be going toward housing to retirement savings and other investments. While owning a home does come with a laundry list of expenditures such as property taxes, maintenance, and interest on the mortgage, it’s clear that in the long run for most Americans, it helps advance their net worth.

Average Net Worth by Age

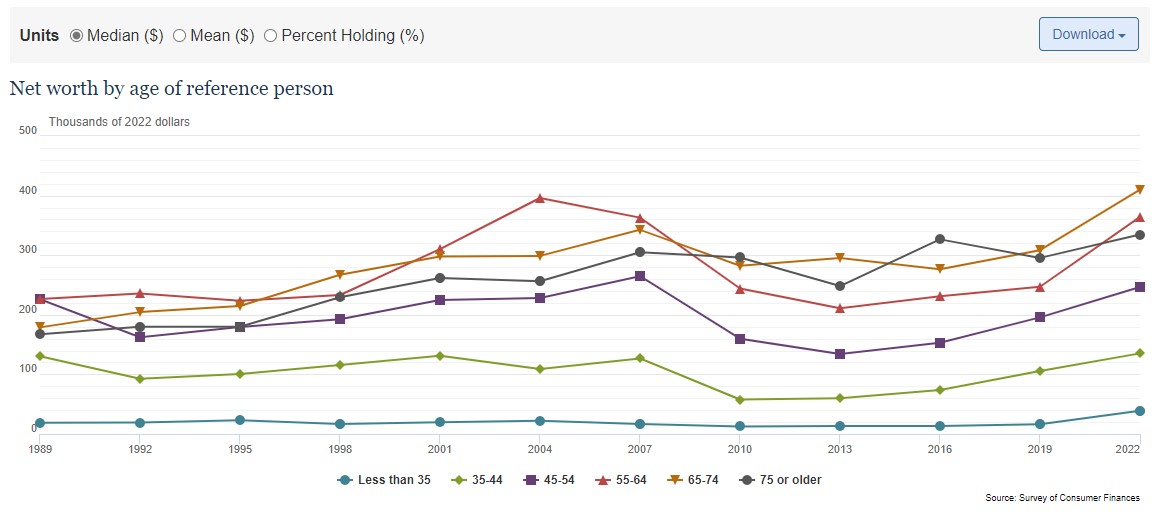

With more years to save and invest, people accumulate a higher net worth. Older people have had more years in the workforce meaning more time to climb the ladder to higher-paying jobs, and for homeowners, allow their property values to appreciate. There is a clear correlation between age and net worth except that people 75 and older have a lower median net worth than those between 55-74. Those 75 and older are likely living off their retirement savings and not focused on replenishing their net worth. You can’t take it with you, so it’s time to kick back and enjoy the golden years.

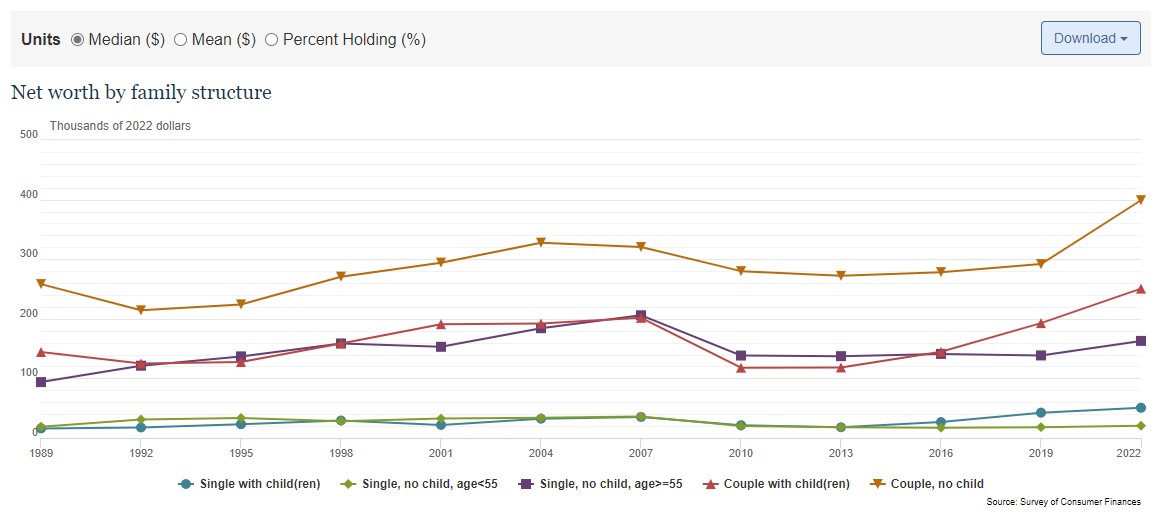

Net Worth by Family Structure

The composition of a family also makes an impact on the family’s net worth. Unsurprisingly, couples with no children have the highest net worth currently and historically. Couples with children surpassed the net worth of single, childfree people over 55 years old and have maintained that trend. Single people with children and single people under 55 years old have the lowest median net worth of all the groups.

This data point speaks to having two incomes compared to one, the cost of childcare (or sacrificed earnings to stay at home and raise children) and how that additional buying power can compound into wealth. Notably, the median net worth of childfree couples is much more than double the median net worth of single childfree people at any age, despite having just double the potential workers in the family.

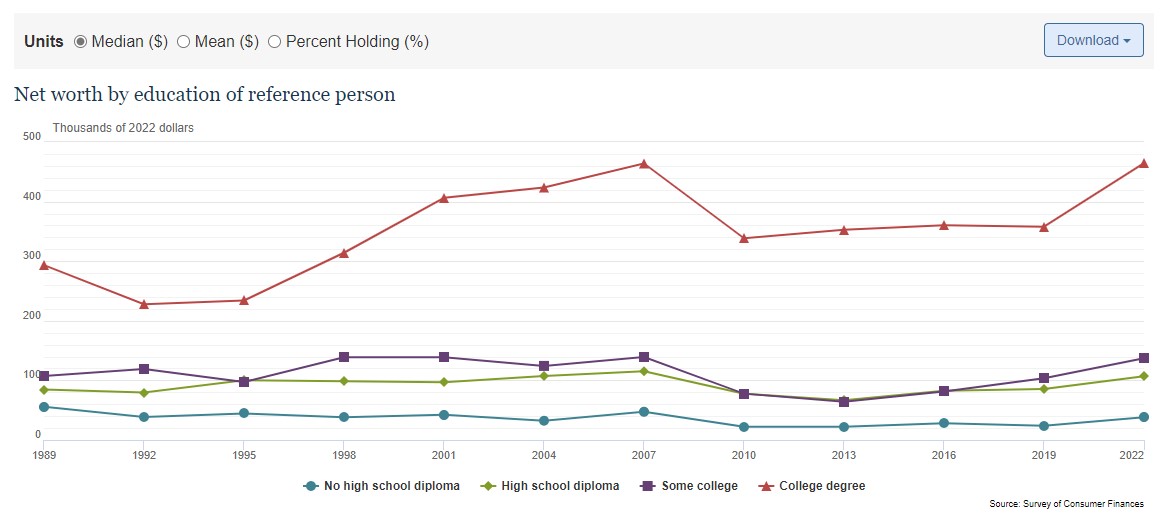

Net Worth by Education

Another important determinant in net worth is one’s education level. Americans with a college degree have a median net worth of $464,400. Americans with some college education have $137,040, a high school diploma have $107,000 and those with no high school diploma have $38,500.

While many well-paying jobs do not require a college education, there is still a correlation with education and higher earnings. Other charts from that survey show that the median gross income for an American family with a college degree is $117,820, more than double the amount from a family where the reference person’s highest level of education is a high school diploma: $52,960.

These higher earnings facilitate access to the other assets that can compound on net worth, such as homeownership or investing in retirement accounts. Americans with college degrees are also more likely to have retirement accounts, stock holdings, pooled investment funds (like mutual funds) and cash value life insurance than others without college degrees. These savings and investment vehicles can help grow the additional income from a higher-paying job into more wealth over time.

Higher education does come with upfront costs and potentially a short-term reduction in earnings. For many, that involves taking out student loans. Be sure to read our blog covering what you need to know about student loans if you’re considering pursuing higher education!

Generational Wealth and Net Worth

Whenever talking about net worth, it’s important to pull back the curtain on the data and acknowledge the role that generational wealth plays. In the 2019 report for the Survey of Consumer Finances, the Federal Reserve noted: “Families can transmit wealth and resources across generations in numerous ways. Families can directly transfer their wealth to the next generation in the form of a bequest. They can also provide the next generation with inter vivos transfers (gifts)—for example, providing down-payment support to enable a home purchase. In addition to direct transfers or gifts, families can make investments in their children that indirectly increase their wealth. For example, families can invest in their children’s educational success, which can, in turn, increase their children’s ability to accumulate wealth.”

Some Americans simply have a head start in net worth or building net worth compared to others. While we covered earlier how investment vehicles are accessible, one must understand them in order to use and benefit from them. Even people who aren’t directly financially supporting their children can pass down financial knowledge to help them make strategic money moves.

Fortunately, one does not need a college degree or an inheritance to have a retirement account, or own stocks or property. Information about what these financial assets are and how to leverage them is more widely accessible than ever thanks to the internet and increased financial literacy classes in high schools. Knowledge is power, and more people can build financial savvy to help make the most of their money and make decisions that will set them up for long-term financial success!

Conclusion

Sometimes, there’s not a simple answer to a question like “how much money do Americans have?” However, by looking at the data in multiple ways, we can find more relevant information to our specific needs and interests. If you’re looking to grow your net worth, it’s clear that getting a college degree and owning a home are two variables within an individual’s control that correlate with higher net worth. (Data shows around 37% of undergraduate college students are first-generation, up from 18% five years prior, which is fantastic progress!)

The Federal Reserve’s website linked above with the survey data is interactive so you can explore what’s most interesting or relevant to you. See how you compare to other Americans based on age, ethnicity, employment status, and educational level to get a better understanding of how you fare amongst your peers.

We applaud you for taking time to build your awareness of the financial status of Americans and hope you gained some meaningful takeaways!

Keep reading on the Milli blog:

Why is Personal Finance Important?

How to Increase Income to Increase Savings

17 Helpful Personal Finance Podcasts