Have you ever thought about what drives your financial choices and attitudes? Psychology plays an important role in our motivations for all action, including our saving and spending.

Understanding the psychology of money is an important factor in the journey to financial well-being. When you can recognize the psychological drivers behind past, present, and future financial decisions, you’re empowered to make informed choices, avoid missteps, and build healthy money habits.

To better understand our relationship with money, we need to dig into our emotions, which are shaped by childhood experiences, and influenced by societal and cultural factors. Taking time to understand the psychology of money can help you navigate financial challenges, build resilience, and ultimately foster a balanced and mindful approach to managing your finances.

Money and Emotions

Money is more than just currency – we have an emotional connection to it. Some feel a positive connection to money, where it’s a tool to help them build a satisfying and secure life. Others associate negative emotions like stress with money – either from not having enough or being uninformed about how to make the best use of it.

The emotional connection to money runs deep and begins forming in your childhood. Research from the Journal of Family and Economic issues published in 2022 shows there is a link between adverse childhood experiences and financial security as an adult. Researchers found that “at various income levels, financial stress in adulthood is related to childhood trauma” because it impacts the brain’s development. The study included traumas that were both related and unrelated to finances. Though you can’t go back in time, it’s valuable to understand and keep in mind that what you experienced as a child made an impact on your psychological approach to money.

The reverse is also true; your current financial situation can impact your psychological wellbeing. Research from the same journal article reviewed data from the Consumer Financial Protection Bureau, which through the Behavioral Risk Factor Surveillance System study found that financial security is an indicator of financial wellbeing, which includes psychological aspects. So, while having money doesn’t solve problems, having the financial security of being able to meet your needs (and ideally thrive) can contribute to your psychological wellness – no surprise there.

Emotions also play a big role in our day-to-day spending and saving choices. Overjoyed at a new baby in the family? Feeling down after a breakup or stressed about work? We have all made financial choices as a result of how we feel. However, if you spend as a coping mechanism for your feelings, that’s emotional spending, and it may not be serving you or your money. Check out our blog on emotional spending to dig in more and find tips for how to address it!

Money and Happiness

Can money make you happy? It’s not a clear-cut answer. In the journal article we mentioned earlier, researchers reviewed the CFPB study and found that someone’s financial wellbeing is not strictly correlated with their income. Other research finds there is some correlation – it supports the idea that happiness and money are somewhat related to a point.

A widely cited study from 2010 found that happiness leveled off at an annual income of $75,000 – which is $106,000 in 2023 dollars, adjusting for inflation. It seemed to make a point – once you have enough money, you’re set. Though, a specific dollar amount goes further in some places than others. $106,000 will get you a vastly different lifestyle in a Midwestern suburb compared to a coastal metropolis.

The plot thickens, though, with new research from 2022 including one of the same economists from the 2010 study. This report found that most peoples’ happiness rises with income, but flattens for some around $500,000 of income. That seems to make sense because anywhere in the United States, half a million dollars will give you plenty of freedom of choice and leisure spending.

Another interesting concept to further your understanding of the relationship between money and happiness is the hedonic treadmill. It’s an idea in psychology and economics that most people have a baseline level of happiness, and people will quickly return to that relatively stable level of happiness or satisfaction after experiencing major positive or negative life changes. And, over time, people will experience less and less impact from the new circumstances.

For example, if you get a new job with a significant increase in income, you may initially feel a boost in happiness and life satisfaction. However, as you become accustomed to the higher income and the things it can get you – stability, material goods, and the freedom of choices – the happiness from the increase in income begins to fade. Eventually, you’ll settle back into how happy you were before the big income jump. The hedonic treadmill explains why happiness doesn’t come from wealth or material possessions.

Ultimately, while it’s not as simple as money in the bank means having intrinsic happiness, we know money is a resource that can help you meet needs. Having your needs met can bring about a sense of security and prevent negative emotions like stress and sadness, which can allow someone to find happiness and satisfaction in other ways in their lives.

Financial Stress and Mental Health

Our psychology can impact how we approach money, and the same goes in reverse: finances can impact mental health. One 2023 study of adults in the United States found a correlation: “higher financial worries were significantly associated with higher psychological distress.”

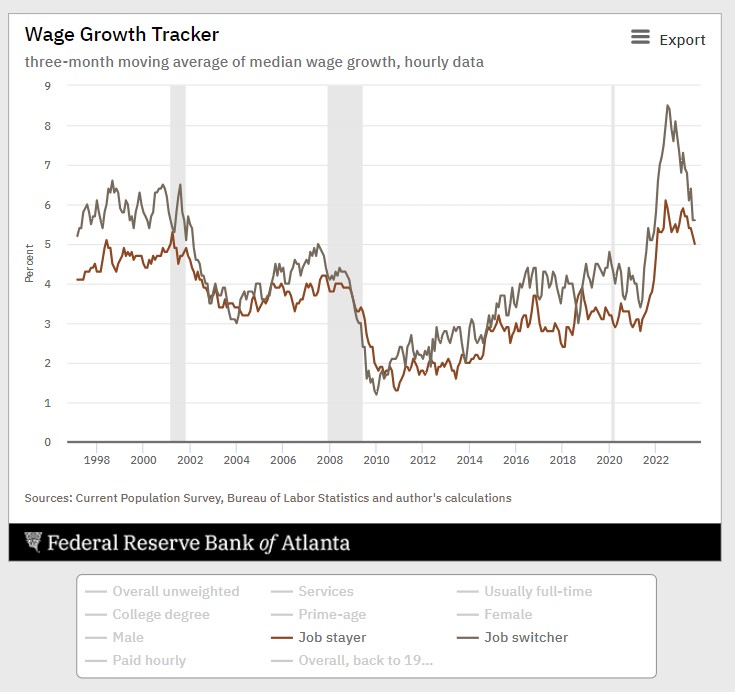

We’ve covered that money can’t bring you automatic happiness, but it can aid in reducing financial worries and in turn minimize psychological distress from that source. Each person and family’s financial situation is unique but having additional disposable income can help most people. That means some people may find it worthwhile to find a new job. Data from the Federal Reserve Bank of Atlanta shows that job switchers tend to have higher wage growth than people who stay in their same jobs.

There’s more good news: people are getting raises, and the majority of people that ask for one are successful. According to the Federal Reserve’s 2022 Survey of Household Economics and Decisionmaking:

- One third of adults received a raise or promotion in 2022 (increased from 30% in 2021)

- 13% of adults asked for a raise or promotion

- Of those people who asked for a raise, 70% of people received one

If you’re looking for new opportunities, check out our blog about ways to increase your income. While it can be challenging and time consuming to solve financial problems, it is worth the effort to keep making progress because your income could increase, and in turn contribute to more positive mental health.

Mindfulness in Money Management

At its core, mindfulness involves being fully present in the moment, acknowledging your thoughts and feelings without judging yourself. What does that have to do with money? Mindfulness is important in finance because it offers a way to stay intentional in your decision making by paying attention to what’s driving your decisions.

The mind is a powerful thing. Researchers from Johns Hopkins reviewed over 18,000 studies and found a link between mindfulness meditation programs and reduced anxiety and depression. It wasn’t overnight – it took eight weeks, but two months of mindful meditation (which costs nothing) to feel less anxious is worth a try. If you can reduce these negative feelings in your life, you may be less inclined to make emotionally driven purchases.

Trying to be more mindful about your money? Dig in to gain awareness of your spending habits, saving goals, and the emotional triggers influencing financial choices. Be mindful when making purchasing decisions and combat cognitive biases that can cloud your judgement. Work toward using your money to build a life that brings you true satisfaction and joy – whatever that looks like for you! With practice, you’ll build financial resilience and foster a healthier relationship with money.

Cognitive Biases in Money Management

The human brain is incredible, but imperfect, and cognitive bias is one example of why. The Cleveland Clinic cites psychologist Kia-Rai Prewitt describing cognitive bias as mental shortcuts based off of previous knowledge to help us categorize information. Our brains process tons of information every second and have a treasure trove of prior knowledge and experiences to shape us. These mental shortcuts don’t always serve us well, because we don’t always have the right information.

It can be hard to overcome our ingrained thinking even in the face of rational thought or clear data – especially when it comes to money, since we hold such an emotional connection to it. Let’s dig into a few cognitive biases that relate to money so we can confront them and make stronger, more informed financial decisions.

Time Discounting

Time discounting makes us value what’s in front of us more than future rewards. If you’ve ever preferred smaller, more immediate rewards over larger rewards you must wait for, you’ve experienced this.

When it comes to money, this can impact your spending and be a barrier to saving up for future purchases. Having something cool now feels more satisfying to our brains than having the same thing (or even a better thing) in the future. But then when it comes to saving up for big expenses or future rewards, like buying a house or saving for retirement, it can be hard to get motivated.

To overcome this, it takes discipline and also some brain hacks. Start by creating a budget and allocating some discretionary spending money for enjoying now and savings for the future, so you know you’re always working toward your goals. Then, make saving fun and gratifying. Use a Milli Jar to set a goal, automate saving, and visualize your progress!

Anchoring Bias

Anchoring bias happens when you base a decision or judgment based on the first piece of information you see – that’s the “anchor”. When it comes to money, anchor bias comes up when making purchasing decisions.

Let’s say you are shopping for a new computer, and the first one you see when starting your research is advertised for $1,000. Computers can cost more or less depending on the specs. But seeing the first one anchors your perception, so computers that cost less may seem like a great deal while computers that cost more might seem like too much.

Whenever you’re shopping for something that’s a bit of an investment, combat anchor bias by remembering that the first price you see doesn’t make it more accurate and do research on the aspects of the product or service and how they match up with your needs.

Status Quo Bias

With status quo bias, people tend to prefer the current state of affairs and resist change, even when a change might be a better move. Researchers from Harvard University and Boston University explain the status quo bias as rational decision-making in the face of uncertainty, regret avoidance, or desire for consistency.

In finance, that might look like resisting change when it comes to your current financial plans or investments, even when it’s clear a different approach could lead to a better result. If you experience status quo bias, you may stick with your current savings and spending habits, even if you could save more money or make more efficient financial choices. This can result in missed opportunities for a higher Annual Percentage Yield on your savings, lower fees, or better investment returns.

Do research on the best opportunities for your money, and if you see it’s worthwhile to make a change, carve out the time to do it. Sometimes just a few minutes and willingness to make a change is all it takes!

Sunk Cost Fallacy

The sunk cost fallacy involves making decisions based on how many resources like time, money, or effort that you’ve already invested in something, rather than considering the current and future value. So even if it would rationally make sense to cut your losses, you may hold onto something because you’re putting more value on the resources you can’t recover.

If your thinking follows the sunk cost fallacy, you may refuse to sell a vehicle or an investment property that keeps needing costly maintenance, or a stock that won’t recover after the share price dropped. It’s hard to let go and walk away because it means accepting a financial loss. Whenever you make financial decisions around parting ways with something, remember that most items don’t last forever, and not every investment is guaranteed to go up. (If your loss is a capital gains loss, look into tax-loss harvesting to recoup some of it back at tax time).

Reframe decisions around how much time, effort, or money something will take going forward so you can keep making the most of resources you already have.

Conclusion

By understanding psychology and how it relates to money, we can reflect and garner a richer awareness of the role money plays in our lives, and how we use it and make financial decisions. Money can’t bring us intrinsic happiness, but it can help us meet our needs so we can find joy in other ways. By being mindful and combating cognitive biases, you can work to make progress toward reducing financial stress and feeling empowered with your money.

Keep reading on the Milli blog:

8 Money Myths: Busting Financial Misconceptions

The Five Components of Financial Literacy

Top Banking Terms You Should Know